Japan’s outward FDI under geopolitical uncertainty

Japanese firms continue to internationalize through greenfield investments, mergers and acquisitions, and equity investments, placing the country as among the top 10 sources of global outward foreign direct investments (OFDI) since the 1990s. Japan peaked as the third-largest source of outward investments between 1992 and 1994, and despite the country’s slow economic growth and aging population, its OFDI stock increased to USD 1.95 trillion as of 2022, ranking seventh highest globally. However, shifting geopolitical issues and evolving global supply chains have reshaped the landscape of international investments, with countries like China rising as one of the biggest investors.

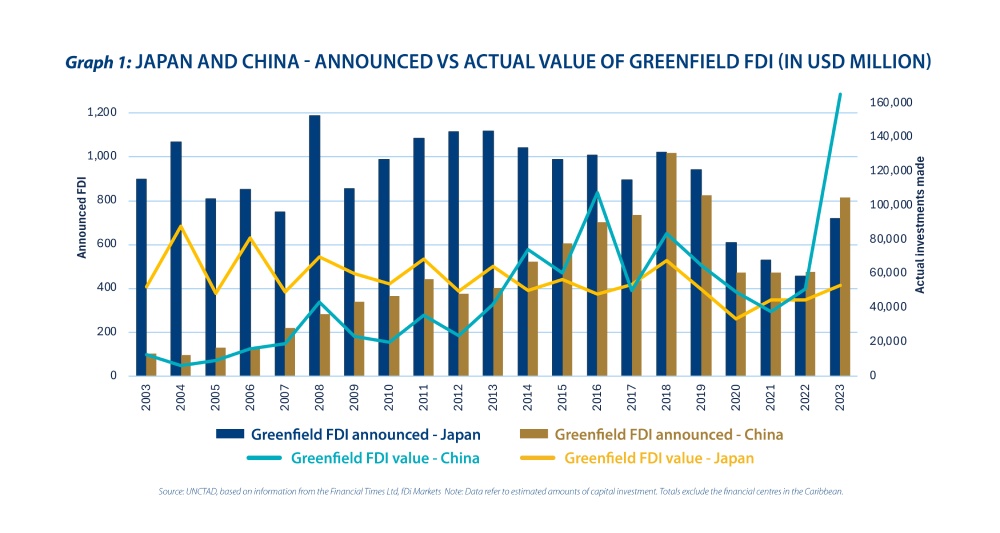

One of the most notable aspects of Japan’s OFDI is greenfield investments, which allow companies to set up full operations abroad. In Graph 1, the years 2003 to 2019 saw more than 800 new greenfield investments from the Japanese annually, reflecting the commitment of Japanese businesses to expand their presence in foreign markets. However, the number of OFDI announcements has declined beginning 2020, partly due to pandemic disruptions. Japan had over 24,000 foreign affiliate companies as of 2022, a product of years of offshore expansion plans over the past two decades.

A new Asian giant

Comparing the trend of outward greenfield FDI for Japan and China provides a broader perspective on the changing dynamics of global investments, particularly in Asia. Historically, China has been known for attracting significant inward FDI due to its comparatively cheap but skilled labour force and level of infrastructure development relative to other developing economies. However, since adopting a “relaxed” OFDI policy in the 2000s, China has significantly increased its overseas investment footprint to emerge as the third largest global investor, breaching USD 2.93 trillion in 2022.

While Japan was consistently ahead in the value of announced investment plans, China has closed the gap in recent years, even surpassing Japan in 2022 and announcing an addition of almost 100 new overseas establishments by 2023. Despite Japan’s lead in the number of new offshore investment projects over the years, the value of China’s investment has exceeded that of Japan’s since 2014. By 2023, China out-invested Japan by over USD 100 billion in new investments abroad, making China the largest greenfield investor from Asia.

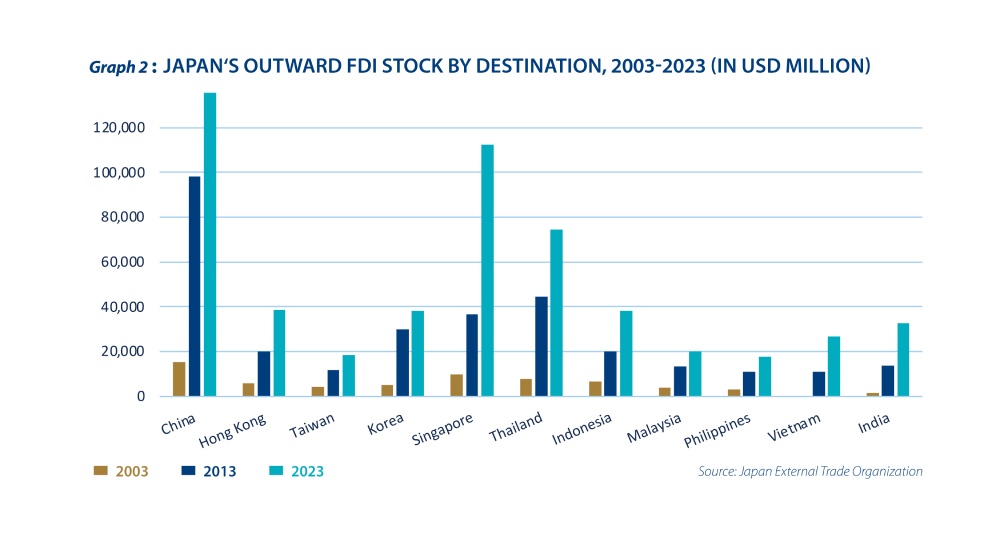

In terms of investment destinations, Japan’s OFDI is more regionally diversified, as only 26 per cent of its investment stayed within Asia. Graph 2 illustrates that the stock of Japan’s OFDI in Asian countries, wherein China still received the largest share in 2023. However, investment into several ASEAN economies has increased significantly. Meanwhile, over a third of Japan’s OFDI went to North America, with 96.5 per cent invested in the US as of 2023.

Japanese affiliate firms, especially in ASEAN countries, have also performed strongly. These firms have employed over 5 million workers, deepened spending on research and development and capital investments in manufacturing, and contributed significant profits especially for non-manufacturing businesses. This gradual shift in investing more towards ASEAN economies highlights Japan’s evolving market dynamics and geopolitical considerations.

Motivations vary

Japan is traditionally recognized for its manufacturing excellence; thus, one might expect the country’s OFDI to be dominated by high-tech manufacturing. However, data from the Japan External Trade Organization showed a notable shift, with non-manufacturing OFDI exceeding manufacturing investment since 2008. Between January-September 2024, non-manufacturing investments accounted for over 70 per cent of total outbound FDI. Finance and insurance emerged as the largest sectors, followed by wholesale and retail as well as communication technologies. These suggest that Japan is making headway in terms of trade facilitation, and in investing in export-oriented supply chains.

In contrast, China’s investment strategy increasingly focuses on emerging markets. In 2023, nearly 70 per cent of its investment stayed within Asia while investments to the US only accounted for about 3.7 per cent of the global total. One can observe that China’s strategy is likely shaped by geopolitical factors. For instance, in 2018 – the first wave of heavy tariffs imposed by the US on Chinese goods – China appears to have redirected investments towards what they deemed as politically neutral or strategically located “connector” countries like Mexico and Vietnam. Still, some high-value investments by Chinese firms went to countries with advanced technology and human capital, regardless of political distance.

Benefits to home

The implications of the outward FDI strategy of Japan are multifaceted. On one hand, there are concerns about a potential hollowing out effect on domestic manufacturing. Between 2000 and 2014, Japan’s OFDI is found to have reduced domestic production, which raises concerns on job losses. On the other hand, OFDI also enhances employment in Japan’s services sector, indicating that non-manufacturing OFDI mainly strengthens the domestic services sector.

To add, the strong performance of Japanese affiliates abroad has generated high returns for investors, with dividends and royalties to Japanese investors exceeding JPY 6 trillion (USD 42 billion) in 2022, especially from wholesale trade. For investors, Japan’s OFDI pattern provides key signals about market opportunities and risks. The diversification of investment across regions and sectors reflects the country’s strategic adjustments to global economic shifts, hinting at discerning yet agile decision-making.

Trade tensions between the US and China create both opportunities and risks for Japanese investments. We previously alluded that Japanese firms may try to navigate Trump’s mega tariffs by increasing FDI placements in the US to benefit from potential price hikes, as well as by diversifying its position across emerging Asia. Thus, investors looking to navigate growing geopolitical tensions and economic uncertainties should closely monitor where Japanese capital is flowing, as these movements provide valuable insights into promising markets and strategic realignments.

This original article has been produced in-house for Lundgreen’s Investor Insights by on-the-ground contributors of the region. The insight provided is informed with accurate data from reliable sources and has gone through various processes to ensure that the information upholds the integrity and values of the Lundgreen’s brand.