The European Central Bank will be busy

The European Central Bank is behind in hiking interest rates, though more work might arise since spontaneous energy crises can also create unexpected hyperinflation periods during the rest of this decade.

The annual symposium for central bankers in Jackson Hole, Wyoming, USA, was back in full force over the weekend of 26th to 28th August. The stock markets felt its full returning force when US central bank chairman Jerome Powell once again stated that he will raise interest rates until demand and growth subside in the US.

The European Central Bank (ECB) is traditionally somewhat less outright in its communications, but a couple of ECB representatives at the symposium in Jackson Hole did indicate that the rate hike is coming, and it is only a matter of whether the interest rate rises by 0.50 or 0.75 percentage points on Thursday, September 8th.

As an investor, my assessment is that one must be aware of the distinct differences in the origins of inflation among the major economic zones around the world. What do I mean by that? If one looks back in economic history, periods of high inflation rarely occur out of the blue, they are man-made through monetary and political decisions. In order to regain control of inflation, it requires self-awareness about own wrong-footed decisions taken at both central bank and political level. Some measures must also be implemented to deal with the causes that generate inflation, which will hopefully bring it under control.

It is clear to everyone that inflation is raging in the US and Europe, but there are clear differences in both situations on each side of the Atlantic. The US economy is back, in a potent version with a too low supply of labour, which is why the US central bank (Fed) is so aggressive with its interest rate hikes. The Fed is only looking to cool down the economy and I am confident that it will succeed.

Here, the central bank is ready to take a recession into the bargain, which clearly worries investors. The Fed has acknowledged that it did not understand the strength of the US labour market, nor the extent to which people were leaving the labour market. It has become clear now, and my expectation is that the US economy will get back on track through the current tough monetary policy cure.

The ECB does not need to raise interest rates to cool the economy because the recession will probably come on its own. With this, the Eurozone once again risks exposing the structural economic problems that plague what is still one of the world’s largest economic zones.

This is where self-awareness starts to come into play, and it will be particularly interesting for investors to follow how the decision-makers in the Eurozone/Europe deal with self-awareness and solutions to challenges.

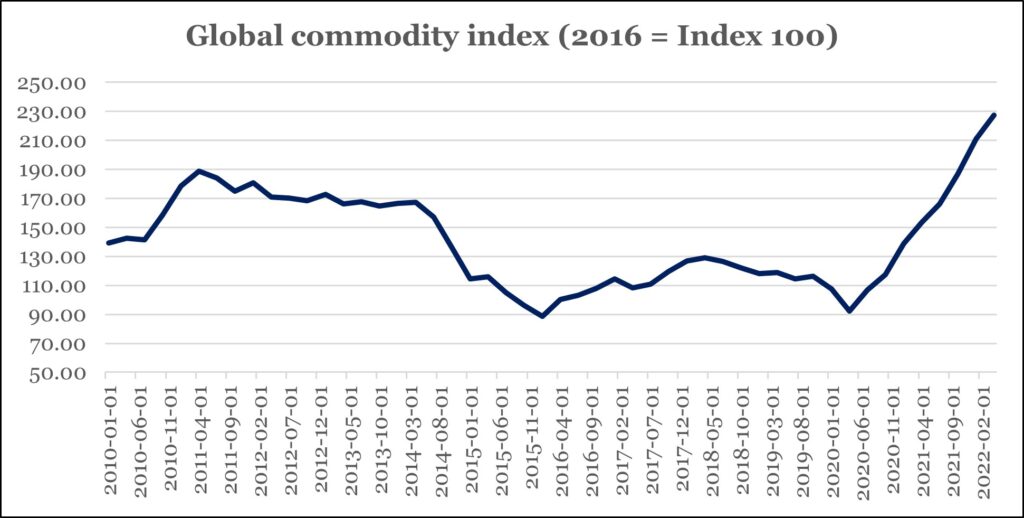

I have noted that, from the political side, it is often mentioned that the high inflation is due to Russia’s war against Ukraine. Immediately, my position is that such statements should be taken with reservation. Graph one shows a global commodity price index that has gone up since the Covid-19 pandemic paralyzed a large part of the world in the first quarter of 2020. On the curve in the graph, one can’t even see the slightest acceleration after the 24th February 2022, the day of Russia’s invasion. This shows that rising inflation has been in the works for a long time. In my estimation, the reason was the numerous shutdowns in the business world combined with the fact that purchasing power was maintained, this phenomenon was pronounced in Europe and the USA.

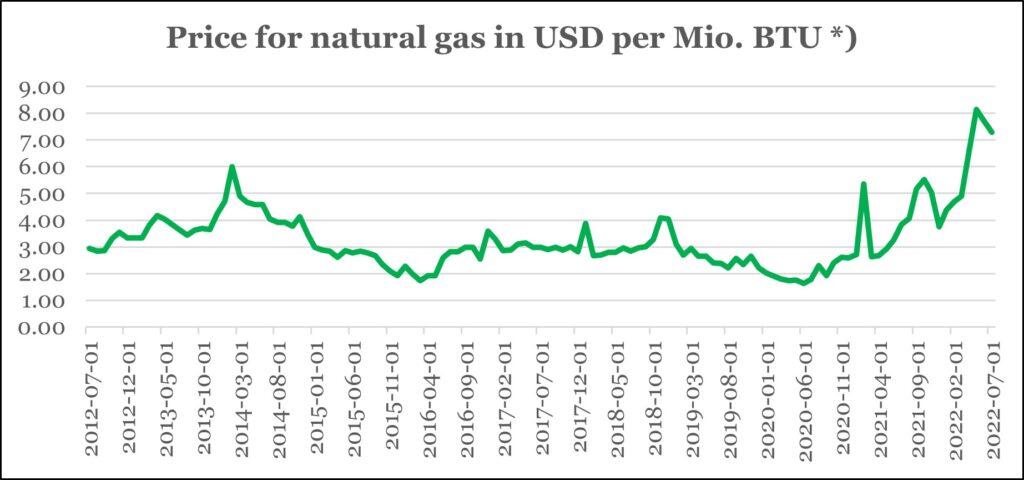

It is also noteworthy to add that crude oil is now trading at a lower price than before Russia’s invasion of Ukraine, the same applies to petrol in the spot market in the USA. The price of petrol at the pump in the USA is eight pct. higher than at the end of February, which is partly seasonal, but not dramatic either. Graph two confirms that the global gas shortage also extends to the USA, which I also expect will burden American households this winter, since heating based on natural gas is widespread in the USA. However, this is only the one major challenge in the American energy supply, which is very different in Europe.

Europe once again ends up with a self-inflicted problem. With the former German political leadership at the helm, the security policy was thrown out of control in order to get cheap Russian gas, the consequences of which, are now being seen.

At the same time, the European leadership has focused heavily on so-called green energy, which is good if it is genuine green energy. But decision takers failed to accept the objections of experts from the conventional energy sector (like oil production). The experts have pointed out for years that there is under-investment in conventional energy production, which means that additional energy cannot be produced if it becomes necessary. Furthermore, the warning has also been that due to underinvestment, conventional energy supplies will not be sufficient until 2030, when green energy is expected to have gained the necessary capacity.

As mentioned, economic history shows that self-awareness is needed before the decision-makers can work on solutions towards the origin of inflation – I don’t know if that will be the case in Europe, but from a risk point of view, I currently assess that the Eurozone/Europe is the economic zone where there is the greatest risk of similar spontaneous inflationary extremes for the rest of this decade, primarily due to the risk of spontaneous energy crises.

Although I am often critical of the ECB, even the most imaginative monetary policy will not be able to cope with this kind of inflation risk. It will be interesting if the ECB brings this theme to the fore, as this is a fully justifiable concern for a central bank.