No Easter egg for investors this year

Here it comes, the inflation, and in particular, the inflation measurable for enterprises. It is the producer prices that are on the rise, which is the price inflation companies experience when purchasing goods and services that are part of the production.

As the general consumer price inflation had an unusually prominent focus in the financial markets during the first quarter, it is my assessment that a sustained increase in producer prices will receive significant attention this coming second quarter.

Changes in producer prices are always interesting- to a certain extent. However, when the general consumer price inflation has been rising for some time, and when producer prices begin to rise in a broad sense, I pay special attention to these developments. It is in such situations that risk arises for a spiralling long-term rising inflation.

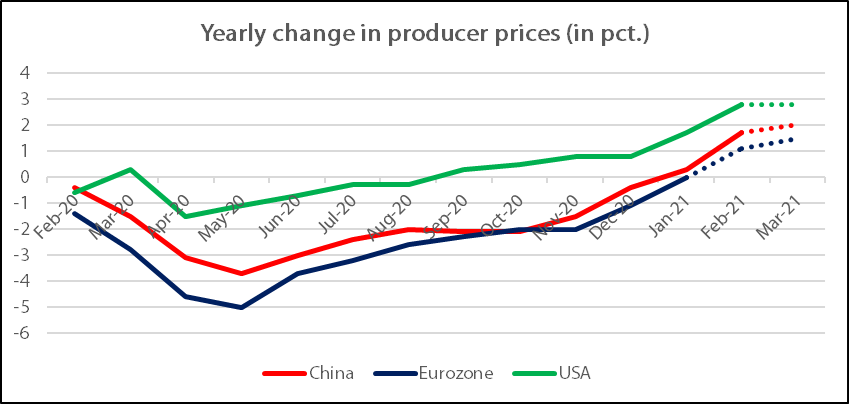

Graph one clearly shows the development in producer prices, and it is global, which I chose to notice. The development may not seem very significant, but the rate of increase has been steepening in recent months. It should also be mentioned that the figures for March in the graph shows the expectations in the financial markets. The excitement about what the real numbers will already be triggered just after Easter, on the 8th and 9th April. The prospect is that the rise in producer prices will continue to remain at a high level. Surely, if one, as an investor, is worried about higher inflation, then there is not exactly an Easter egg awaiting from that front.

In my assessment of producer prices in relation to the financial markets in general, the essential thing about the changes in the producer prices is whether these are pushed through to consumers or absorbed by the enterprises in the production and sales chain.

It is far from usual that producer price increases automatically are passed on to consumers. An all-natural explanation is the competitive situation in the consumer market, and for example, if many agreements between the manufacturer and the retailers have long maturities. This means that price increases cannot necessarily be passed on at any time. But here too, the world is changing, because it is becoming increasingly lean, and concerning logistics, the “just in time” delivery is perfected to the extreme.

With perfected logistics, it encourages developments where producers sell directly to the end consumers. It means that several links between producers and consumers are eliminated, for the sake of reduced costs. One consequence is that higher producer prices are more likely to be passed on directly to consumers in a much greater extent. It is also going to happen much faster than earlier, as the now reduced chain of sales distributors between producers and consumers used to absorb price increases, either partially or as a whole.

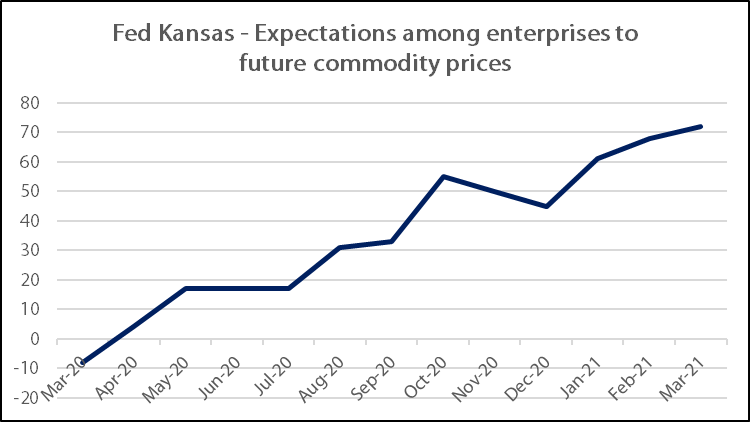

Graph two illustrates how actual this direct impact on consumer prices can become in the near future. The US Federal Reserve Bank (Fed) has divided the US into 12 regional areas, each represented by a branch of the central bank. The Kansas branch covers six states in the midwestern United States, and each month, a number of companies are asked if they think commodity prices are higher or lower in six months’ time. Here, the graph indicates an outright dramatic development and other regional branches of the central bank have similar measurements that show similar expectations among companies, with the same significance, though not quite as dramatic.

My assessment is that when the expectations are so strong, there is a higher risk that price increases will be pushed forward to consumers, as the companies simply need to deal with their own expectations. There are reports in the press from a number of companies that price increases this time, will be passed on to consumers, specifically because other costs also are increasing, like transportation. Despite the expectations almost looking extreme, I still think that there is a great uncertainty about how large a share of the price increases actually will end up as inflation for the consumers.

Am I worried? No, not more than the increased attention to the prospect of rising inflation, which has already been the case during first quarter. My assessment remains that the primary reason for the rise in inflation can be explained by the global economy moving forward again. It has now been recognised by many investors that the US inflation can reach 2.5 pct and the 10-year interest rate in the US has now risen to the expected 1.75 pct.

If I must point out a direction for my concern level, then it has increased slightly, yet not more. It is, of course, worrying with the prospect that companies may pass the bill on to consumers this time, so the situation with rising inflation drags on. In the case of the United States in particular, I would not deny that the large coming economic stimulus package will also cause inflation somewhere down the timeline- this is the risk that former U.S. Treasury Secretary Lawrence Summers stated a few months ago.

I am very aware of the risks mentioned, but currently, my position is that it is still too early to be overwhelmingly concerned about this potential risk. My position remains that the possibility of inflation calming down, after the increase during the coming period, is still as big as the risk of the high-level inflation to continue.