Inflation is now taking control

All economic growth forecasts are now being lowered once again, which will naturally increase uncertainties in the financial markets.

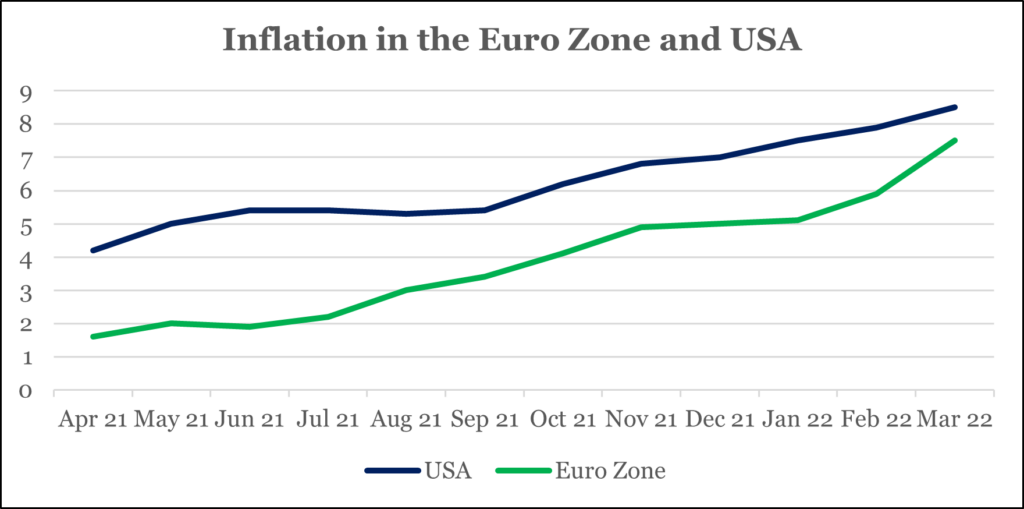

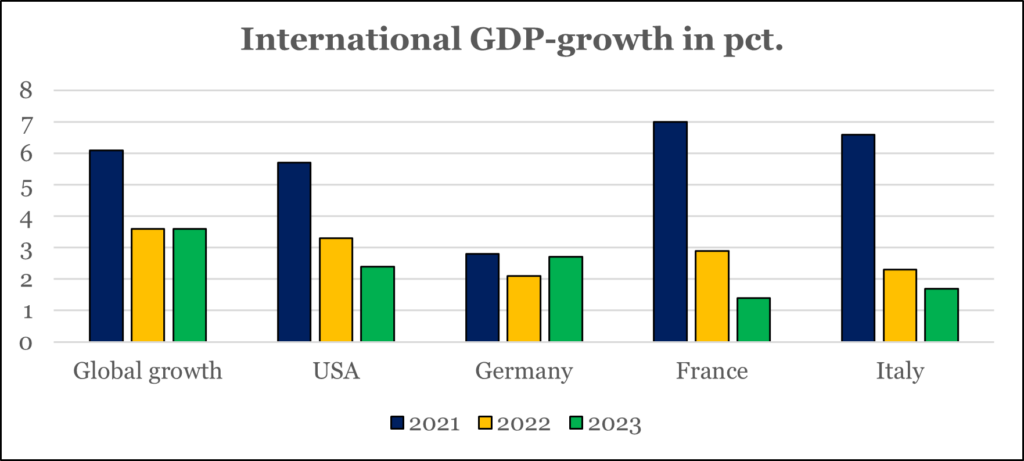

On Tuesday, 19th April, it became as official as it could be, that the global economy is facing a significant decline in growth rates. The International Monetary Fund (IMF) announced its revised expectations for the GDP growth around the world, and as graph one indicates, inflation continues its perpetual rise, while graph two shows the IMF’s new expectations for the GDP growth – these two developments can only result in a bad economic cocktail.

My assessment is that since before the global financial crisis in 2008, the global economy has found its upwards momentum based on an economic and monetary policy of patchwork solutions. The overall risk that investors are experiencing right now is whether it has come to an end, and if the fundamental global macroeconomic market forces have taken over its own regulation of the large imbalances that have built up over the years.

It is obvious that Russia’s war against Ukraine contributes even more to the imbalance. Energy prices have risen sharply, some raw materials can no longer be imported from Russia, and wheat and sunflower oil from Ukraine are absent. In addition, some companies are affected by the fact that outsourcing to these two countries has been interrupted, and that once again, there will be halts in the regional supply chains. Russia and Ukraine also account for large supplies of fertilizers, which will have an effect on agricultural costs in several parts of the world. The war is also very close to Western Europe, which dampens the desire to invest and consume in a number of large European countries.

It is not without reason that the IMF downgrades global growth in the wake of the war. However, if one takes into consideration that Russia’s economy is not much larger than Spain’s economy, and Ukraine’s economy is somewhat smaller, then a fall-out of the two economies does not seem like something that should threaten the overall global economy.

The aforementioned factors illustrate that Russia’s war against Ukraine has a global reach, and therefore, the war affects the world economy more than one might would think. However, even if one corrects for the entire global economic impact of Russia’s war on Ukraine, then the war is far from the explanation for the overall challenges facing the global economy.

For many years, I have been arguing that the politicians in many countries live with the notion that it is politically possible to regulate all the elements that are part of the very large macroeconomic equations. By “equation” I also infer to a balance because an equation contains equal parts of pluses and minuses on both sides, otherwise it does not go up.

The financial crisis itself led to the invention of the quantitative monetary policy that seriously intervened in the equation. I argue that the economic handling of the Covid-19 crisis has contributed to an extreme imbalance in the equation. The truth is that even before Russia started the war against Ukraine, for example, inflation was already skyrocketing.

The years 2022 and 2023 are quite interestingly also the 100th anniversary of the infamous hyperinflation that ravaged the Weimar Republic (Germany). From June 1922 to December 1922, the general price inflation rose to 1700 pct., and the following year to even more astronomical heights.

Now, I will in no way make a prediction that there will be hyperinflation in the world, but I have earlier drawn parallels to the causes of hyperinflation from hundred years ago, and I believe the parallels are more valid than ever. One reason for the hyperinflation was a sharp growth in the money supply that was not linked to a gold standard. Among several other reasons, inflation rose due to the conflict over the Rhineland. Here, the Germans stopped the industrial production, but the government in Berlin took over the wage payment of all the employees of the companies involved.

One cannot make a full comparison with the Covid-19 crisis, but concerning macroeconomic management, today’s politicians could have learned a lot from what happened 100 years ago. In the economic compensation in connection with the closure of societies during the Covid-19 pandemic, many governments have used, in my opinion, comparable measures.

During the crisis, very large public financed credits were given to the private sector, thus, the increase in the money supply is channeled to sectors where it maintains demand (during the global financial crisis, the money supply was “only” increased in the financial system). The same happened for employees, many of whom have had their wage income maintained despite the fact that the work disappeared fully or partially for a period.

This means that in many western economies, a situation arose where demand was maintained, but output was lowered quite a bit – this contains the germ of uncontrollable inflation. In addition, property prices continued to rise, which for example, meant that in the US, a number of employees have been able to sell their houses and self-retire earlier than expected. It is just one example of employees disappearing from the labour market in the United States, which again, contributes to wage inflation.

My assessment is that in the shadow of the economic effects of Russia’s war against Ukraine, there are very large global macroeconomic forces engaged in a sort of self-regulation, in which politicians have no power over. This may mean that prices can rise until the growth rates drop sharply, just as the IMF’s growth forecast for 2023 predicts – I just hope that growth does not fall into a deep hole.